CMS News

FOR IMMEDIATE RELEASE

February 23, 2017

Market Saturation and Utilization Data Tool

The Centers for Medicare & Medicaid

Services (CMS) has developed a Market Saturation and Utilization Data Tool,

formerly called the Moratoria Provider Services and Utilization Data Tool, that

includes interactive maps and a dataset that shows national-, state-, and

county-level provider services and utilization data for selected health service

areas. Market saturation, in the present context, refers to the density of

providers of a particular service within a defined geographic area relative to

the number of the beneficiaries receiving that service in the area.

The fourth release of the data tool

includes a quarterly update of the data to the eight health services areas from

release 3, and also includes Physical and Occupational Therapy and Clinical

Laboratory (Billing Independently) data. Release 4 will therefore include four,

twelve-month reference periods and the following health service areas: Home

Health, Ambulance (Emergency, Non-Emergency, Emergency & Non-Emergency),

Independent Diagnostic Testing Facilities (Part A and Part B), Skilled Nursing

Facilities, Hospice, Physical and Occupational Therapy, and Clinical Laboratory

(Billing Independently).

The Market Saturation and

Utilization Data Tool can be used by CMS to monitor and manage market

saturation as a means to prevent fraud, waste, and abuse. The data can

also be used to reveal the degree to which use of a service is related to the

number of providers servicing a geographic region. Provider services and

utilization data by geographic regions are easily compared using an interactive

map. There are a number of research uses for these data, but one objective of

making these data public is to assist health care providers in making informed

decisions about their service locations and the beneficiary population they

serve. The tool is available through the CMS website at: https://data.cms.gov/market-saturation.

Future releases may include comparable information on additional health service

areas.

Methodology

The analysis is based on paid

Medicare claims data from the CMS Integrated Data Repository (IDR). The IDR

contains Medicare and Medicaid claims, beneficiary data, provider data, and

plan data. Claims data are analyzed for a 12-month reference period, and

results are updated quarterly to reflect a more recent 12-month reference

period.

The Market Saturation and

Utilization methodology is different from other public use data with respect to

determining the geographic location of a provider. In this analysis, claims are

used to define the geographic area(s) served by a provider rather than the

provider’s practice address. Further, a provider is defined as “serving a

county” if, during the 12-month reference period, the provider had paid claims

for more than ten beneficiaries located in a county. A provider is defined as

“serving a state” if that provider serves any county in the state.

The Market Saturation and

Utilization methodology is also different from other public use data with

respect to determining the number of Medicare beneficiaries who are enrolled in

a fee-for-service (FFS) program. In this analysis, a FFS beneficiary is defined

as being enrolled in Part A and/or Part B with a coverage type code equal to

“9” (FFS coverage) for at least one month of the 12-month reference period.

There must not be a death date for that month or a missing zip code for the

beneficiary so that the beneficiary can be assigned to a county. Other public

use data may define a FFS beneficiary using different criteria, such as

requiring the beneficiary to be enrolled in the FFS program every month during

the reference period.

The Market Saturation and

Utilization Data Tool includes an interactive map that is color-coded based on

an analysis that separates the distribution into the following categories of

states/counties for the selected metric: lowest 25 percent, second lowest 25

percent, third lowest 25 percent, top 25 percent excluding extreme values, and

extreme values. An extreme value is one that greatly differs from other

values in its field (e.g., Number of Providers). For those interested in states

and counties affected by CMS’ temporary provider enrollment moratoria during

the reference periods for which data are available, the interactive map permits

a visualization that identifies those states and counties. In this

visualization, ambulance and home health service areas for moratoria versus

non-moratoria states/counties are also identified based on color scheme.

Counties that are excluded from the analysis are colored gray in the

interactive map.

The examples below utilize the

Ambulance (Emergency & Non-Emergency) service area data (selected for

illustration purposes only). Similar maps can be created through the Data Tool

for all of the health service areas included in the fourth release and for the

four, twelve-month reference periods: 2014-10-01 to 2015-09-30, 2015-01-01 to

2015-12-31, 2015-04-01 to 2016-03-31, and 2015-07-01 to 2016-06-30.

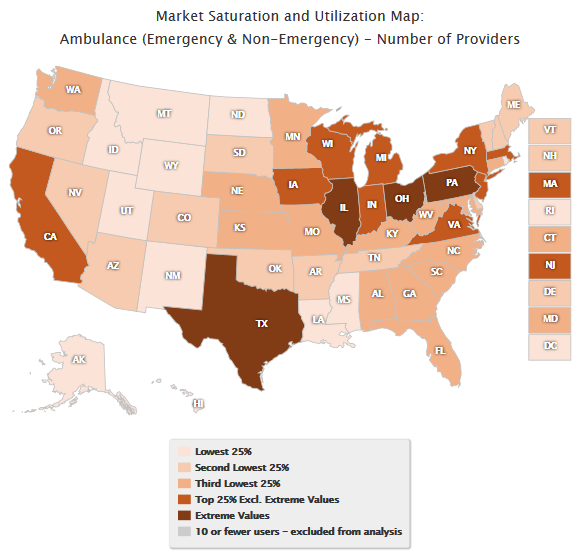

Map 1 displays the distribution of

providers by state for the Ambulance (Emergency & Non-Emergency) service

area for the October 1, 2014 through September 30, 2015 reference period. This

map utilizes a single color scale, which does not distinguish between moratoria

and non-moratoria states.

Map 1. Ambulance (Emergency & Non-Emergency):

National Distribution of

Number of Providers

October 1, 2014 – September

30, 2015

Single Color Scale

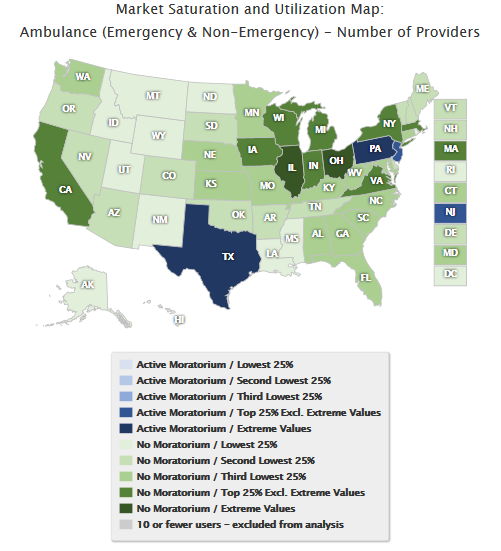

Map 2 displays the

distribution of providers by state for the October 1, 2014 through September

30, 2015 reference period. This map utilizes a dual color scale, which

distinguishes between moratoria and non-moratoria states.

Map 2. Ambulance (Emergency & Non-Emergency):

National Distribution of Number of Providers

October 1, 2014 – September 30, 2015

Color by Moratoria Status

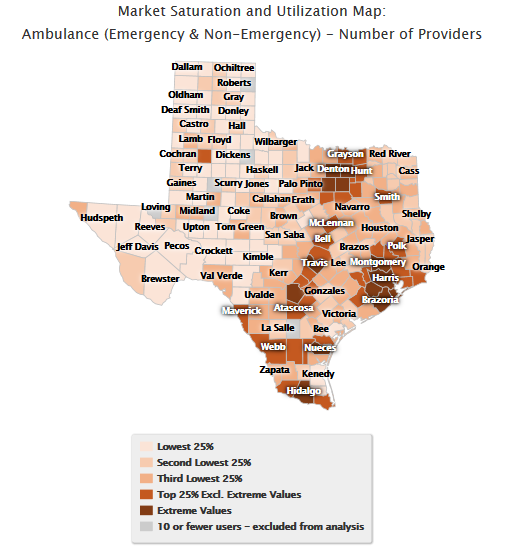

Map 3 drills down to the

county level and displays the distribution of providers by county within the

State of Texas for the October 1, 2014 through September 30, 2015 reference

period. This map utilizes a single color scale, which does not distinguish

between moratoria and non-moratoria counties.

Map 3. Ambulance

(Emergency & Non-Emergency):

County Distribution of Number of Providers

October 1, 2014 – September 30, 2015

Single Color Scale

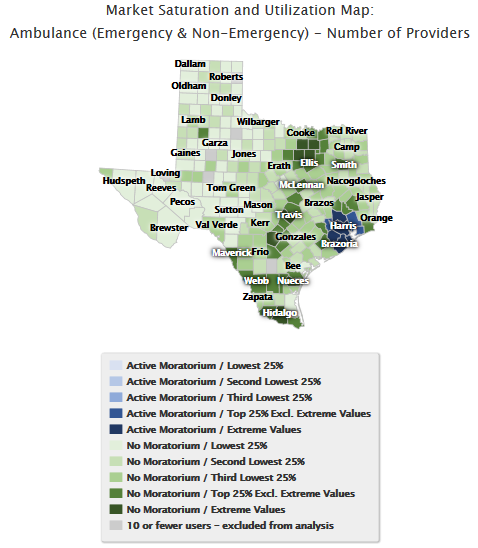

Map 4 drills down to the

county level and displays the distribution of providers by county within the

State of Texas for the October 1, 2014 through September 30, 2015 reference

period. This map utilizes a dual color scale, which distinguishes between

moratoria and non-moratoria counties.

Map 4. Ambulance (Emergency & Non-Emergency):

County Distribution of Number of Providers

October 1, 2014 – September 30, 2015

Color by Moratoria Status

Similar maps can be created

at the national- and state-level for the other metrics included in the Data

Tool: Number of FFS Beneficiaries, Average Number of Users per Provider,

Percentage of Users out of FFS Beneficiaries, and Average Number of Providers

per County.